According to Mr Davies, what advisers need to keep in mind is that product governance in its own right is all about product manufacturers and target market criteria.

He suggests this is because product manufacturers have to factor in the way they build their product features such as benefits, costs and charges, into the client type: the knowledge and experience of the client as well as their ability to bear losses, their objectives, needs and their risk appetites.

Then there are, of course, the distribution channels, or in this case, IFAs.

The FCA provides suitability rules for advisers to ensure that their services, and their products, are suitable to meet clients’ needs.

This is where segmentation comes in because what Prod demands is that advisers clearly segment clients around the outcomes clients are trying to achieve, according to Mr Farquhar.

He explains: “You have to define the target market for the different segments of your centralised investment proposition, at which point you need to really segment your clients and define their revenue and the service proposition you can give them."

Source: Square Mile

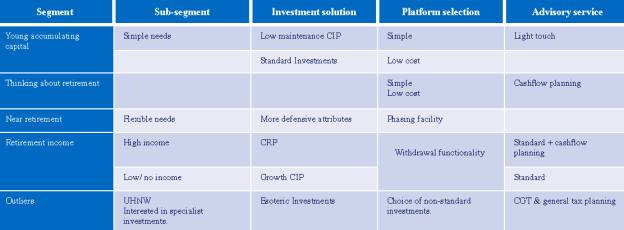

How are advisers segmenting clients?

The way advisers have historically come at segmentation, if at all, has been fairly transactional, according to Mr Davies.

By 'transactional' he means segmenting around two key demographics: age and assets under management.

But in a post-Mifid II environment, that is no longer enough to comply with the requirements, he suggests.

Mr Davies explains: “It will not meet the rules and regulations; it is not going to meet what clients need.”

So what will? These days it is a lot more complex, and he suggests segmenting clients has to be taken from a behavioural point of view.

He continues: “[So] if you segment clients now you also have to factor in whether it is profitable for the business to take on a certain section of clients, different types of technologies, costs and charges – how much you are going to charge each particular section of the clients – and then you also have to factor in and map over the product arrangements target market criteria.”

He adds: “It's not an easy exercise and advisers often think they can approach it transactionally, based on age and wealth, but that is just not going to work.”

According to Jiten Varsani, mortgage and protection adviser at London Money, some advisers segregate based on occupation: teachers, doctors, lawyers.

He says: “Of course there are those who do not have set segregation criteria but may have a minimum fee for any work carried out which in turn could lead to segregation between those with the means to pay and those that cannot afford it.”