The Covid-19 crisis has inflicted a very sharp but short recession on the world.

Governments and central banks have responded forcefully with a bridge to support everyone through the crisis.

As we enter autumn in the northern hemisphere, the strongest part of that bridge is behind us. The section ahead is incomplete.

Bond and equity investors appear to disagree about whether we will reach the other side before looming risks envelope the economic outlook.

Our base case is that a moderately effective vaccine will be approved and made available to billions of people by the end of 2021.

If we are right, a return to relative normality may be possible.

However, before a vaccine can deliver this optimistic scenario, starting perhaps from spring 2021, we must survive winter.

The benefits of monetary and fiscal support have been powerful, but are beginning to fade.

Summer infection rates were low but, as the weather turns colder, people will spend more time in enclosed environments.

Meanwhile, the US presidential election is just days away. Our portfolios reflect our optimism that we will reach the other side of this crisis, although we remain well diversified, should the bridge to spring prove too perilous.

Bridges cost money

Governments worldwide have already provided trillions of dollars in Covid support packages.

For instance, Germany has extended its furlough scheme for another two years. In the UK, the Job Support Scheme will run for six months as of November 1, replacing its furlough programme, which comes to an end on October 31.

Others are less generous. In the US, political disagreements since July have already prevented the renewal of support packages that included an extra $600 (£460) a week in unemployment benefits.

These payments have been critical in boosting US personal incomes by almost 7 per cent, despite almost 12m fewer people on payrolls.

If these support measures are not renewed, US personal incomes may fall by at least 5 per cent.

The resultant hit to economic activity could be substantial. Our view is that, without at least $1tn in new stimulus, the US economy will suffer a serious setback before any vaccine arrives that may support a stronger economic recovery.

Winter is coming

Even before winter sets in, new Covid-19 cases across Europe and elsewhere are escalating. The Centres for Disease Control said in October the virus could be airborne and so is more likely to spread as people socialise indoors over winter.

Already, new localised lockdowns and more stringent social distancing guidelines have been imposed. The economic benefits of opening up after the initial lockdowns could reverse.

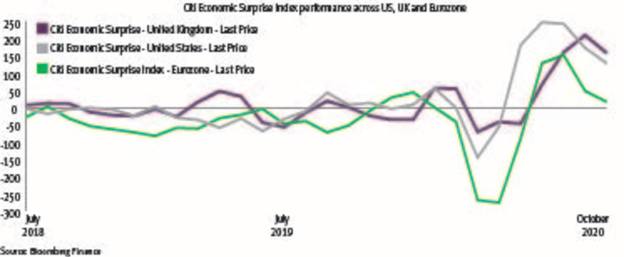

We see this already in weakening ‘economic surprise’ indicators and high-frequency economic activity indicators. Investing is supposedly for the long-term but, for many businesses, another winter of losses could prove ruinous.

The best path forward

Perhaps more than usual, the US presidential election in November has taken centre stage because the two major parties hold such different views of the best path forward.