Prior to 2020, it had generally been considered that it was a bad time for active equity managers.

As equity valuations reached historic highs around the globe, passive and tracker funds soared in popularity, often outperforming their active counterparts.

Nonetheless, the volatility and downturns in the markets caused by the Covid-19 pandemic have offered active managers the chance to demonstrate their worth; conventional wisdom holds that active managers are better able to manage the downturn than a fast-falling tracker.

While looking at returns over the course of the year is often the de facto position for many investors, another way to measure active manager performance is through maximum drawdown.

Maximum drawdown measures the highest peak of a fund’s performance to its lowest trough over any given period of time and can show how active managers can counter the downside.

Given that the US and the UK have faced very different economic and political challenges this year, they present a diverse opportunity to see how active equity managers have been faring.

UK

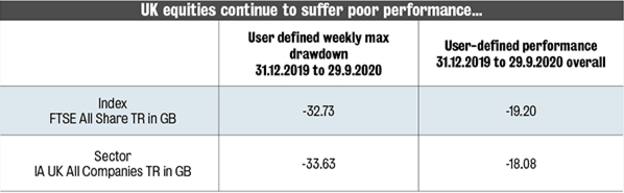

UK equities have – and at the time of writing continue to – suffer from poor performance and related unpopularity with investors.

As the table below shows, active managers have struggled to manage the downside, as the structural problems within UK equities (an overreliance on cyclical businesses and small caps) continue to harm performance and increase maximum drawdown.

Here we can see that the IA UK All Companies sector has suffered greater maximum drawdowns in comparison to the FTSE All Share indexsince March.

Of the best performing funds within the sector, very few active managers have been able to improve upon this drawdown, with the CFP SDL Spirit fund being a rare exception, having seen a maximum drawdown of only -26.58 per cent during this period.

US

If we turn our attentions towards the US, the picture is slightly different.

Largely driven by big tech stocks, which have capitalised on households under lockdown, the Faang companies (Facebook, Apple, Amazon, Netflix and Google) have seen active equity managers perform much better over the same time period, as the table below shows:

While the IA North America sector may have returned less (7.22 per cent) than the S&P 500 (8.07 per cent) since the start of the year, the maximum drawdown that investors in the sector would have suffered would have been less (-22.66 per cent) than those invested in an S&P500 tracker fund (-24.31 per cent) during the same period.

At fund level, Morgan Stanley’s US Growth fund has been the star performer, returning 91.16 per cent over the course of the year, with its maximum drawdown standing at -21.99 per cent.

As we have seen throughout 2020, almost every sector is liable to sudden volatility.

Although it can be easy to look at returns as the only measure when evaluating performance, in the tricky situation of a downturn, maximum drawdown can reveal a whole lot more.