The chaos that engulfed markets in March answered one of the great puzzles that had bewitched investment professionals over the past decade, but left several other questions unanswered.

As investors stared at the sea of red that swept across their screens with the pandemic bringing pandemonium to asset prices, a sliver of light emerged from the darkness, as the prices of most developed market government bonds rose stoutly when March gave way to April.

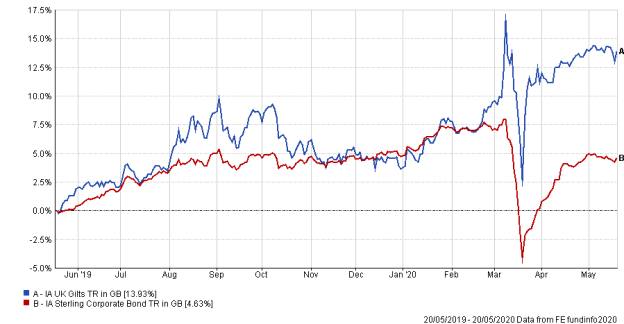

Data from the FE Analytics shows the Investment Association UK Gilts sector produced a positive return of 4.2 per cent for the months of March and April.

And, to an extent, that is the great bond market question answered.

Traditionally, the role of government bonds in a balanced portfolio is to be a diversifier from equities, and to rise in value when equities fall.

Government bonds

Government bonds tend to rise in value at times of severe market stress as investors rush to them as a safe haven, reasoning that the government will always have the cash to pay investors, even if the private sector is collapsing.

In addition, the fact that most global financial services companies, such as banks and insurers have to hold some government securities for regulatory reasons means there is always liquidity in those assets, so they can be quickly sold off in times of strife.

The question mark that dangled over the above hypothesis was whether, given how bond prices had risen sharply and consistently in the decade prior to the financial crisis, there was any room for government bond yields to rise further.

Andrew Hardy, co-head of research and a portfolio manager at Momentum Global Investment Management says government bonds will “always have a part to play” in portfolios because of the regular cashflow and liquidity.

Sebastian Mackay, multi-asset investor at Invesco, says UK and US government bonds had plenty of room to move upwards in price as they continued to trade at lower levels than Japanese and many Eurozone government bonds.

The bonds of those countries have traded at lower yields, and so higher prices, than their UK and US equivalents for a decade because the market expected those latter named economies to grow at a much faster rate than those of Japan and Europe, and so investors were more willing to hold the equities.

But he says the Covid-19 economic shock is such that “it has moved the UK closer to Japan in terms of outlook” and so government bond demand has risen.

A central driver of demand in all parts of the market is the vast programme of bond-buying being undertaken by central banks.

As FTAdviser has previously reported, the specific aim of such bond buying is to push bond prices upwards, and increase liquidity.

Dean Cheeseman, a multi-asset investor at Janus Henderson, says it took the instigation of another round of this bond-buying to make government bonds perform well.