There are fewer more contentious issues in the world of wealth management than the fees charged to clients for the management of their portfolios.

Increased scrutiny from regulators, from clients and from the media around value, transparency, and simplicity over recent years underlined the need for a disruptive approach.

One answer could lie in a low-cost, capped pricing model that treats all clients in the same way – no matter how much money they are investing.

After years of growing concern, costs across the entire UK investment industry were called into question in 2017 when the Financial Conduct Authority published its Asset Management Market Study.

The regulator concluded that price competition was weak in many areas of the retail market with firms enjoying high levels of profitability – average profit margins came in at 36 per cent for sampled organisations – to the ultimate detriment of their clients.

The focus on wealth management fees increased further last year with the publication of the latest edition of EY’s Global Wealth Management Research Report.

The work found that nearly half of discretionary wealth management clients were dissatisfied with fee levels.

This dissatisfaction, which was even more prevalent among younger clients, was found to stem from a lack of clarity around what fees are charged and how they are charged.

EY’s recommendation is clear: firms must recalibrate their pricing models and do a better job of communicating their value to clients.

A need for change

This growing discontent is unsurprising given the traditional wealth management pricing model.

As with many other areas of investment, costs rise as a percentage of overall portfolio size. Clients pay more as they get wealthier.

In a situation where the level of service increases in line with assets invested (where larger portfolios receive a more bespoke service managed by more senior investment professionals) this model can be justified to a degree.

But in a case where one client with a £10,000 portfolio and another with £100,000 receive precisely the same service, there is no justification for charging the latter ten times as much as the former.

From a financial adviser’s perspective, penalising wealthy clients in this way makes it all the more tricky when it comes to demonstrating overall value. The last thing an adviser wants to do is put people off saving.

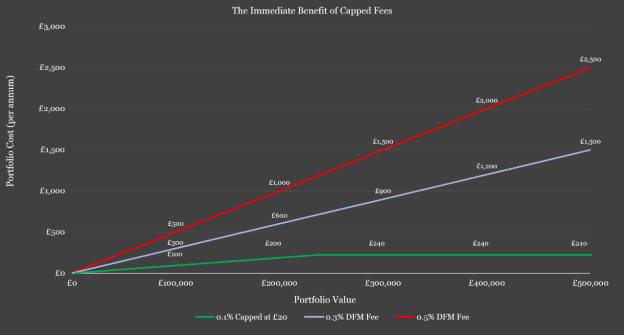

A capped fee portfolio management proposition offers a simpler, transparent, and fair approach when it comes to charging wealth management clients. The immediate and positive impacts of a capped model are demonstrated clearly in the graph below.

Chart 1: shows the first year cost in 10bppa steps for different size portfolios.

It underlines the cost benefit of a capped fee proposition