According to Phil Jeynes, head of sales and marketing for UnderwriteMe, part of the problem is getting enough information from the potential policyholder in the first place.

He says: "The biggest difficulty is in eliciting enough information from a customer to determine whether they have mental health issues which present a genuine underwriting risk, or whether they deal with stress as a natural part of life, like all of us, but are lucky enough that it never impacts on their lives to a significant degree.

"Inevitably, point-of-sale underwriting can only give you a snapshot of a person’s life; we can see the past quite clearly and can make educated guesses about the future, but they remain guesses nonetheless."

However, he says the types of question insurers ask are evolving to deal with this better and get a fuller picture of the customer, and this, together with the adviser's own questions and explanation, can go a long way towards helping people get the cover they need.

Assessing individual cover

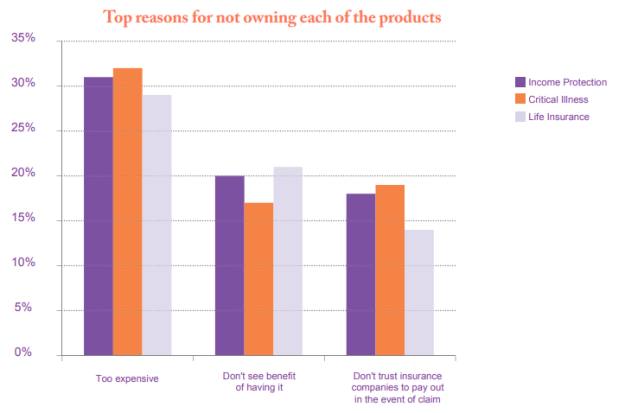

There is also the question of 'will it pay out'? Some people just do not think it is worth the price. As Royal London's State of the Protection Nation report showed last year, most people want to protect their families financially, but do not believe insurance policies are the way to do this.

Figure 1 shows the main reasons given for not taking out life insurance, income protection or critical illness cover.

Figure 1:

Source: Royal London

Some of the perceived problems cited by the Royal London research may not necessarily just be in the person's head when it comes to mental ill health conditions, says Alan Lakey, founder of CI Expert.

He believes while protection is crucial to help people, there has been a historic lack of product development and decent terms for people with mental ill health.

Mr Lakey explains: "There seems to be a knee-jerk reaction with underwriters where any indication of historic anxiety/stress/depression involves excluding future claims for related conditions (including ME).

"It also appears to many advisers that underwriters treat event depression - such as being depressed due to the death of a family member - the same as clinical conditions.

"This certainly seems an unfair methodology."

Advisers therefore have a doubly difficult role: to encourage clients to take out much-needed cover while also making sure the provider will not penalise the client for having any previous history of stress or depression.

Providers are aware of this and have been making efforts to improve the scope of their cover for policyholders with mental ill health, especially considering mental health conditions are not always permanent and can be treated successfully.